Mad-Money-Backtesting

Recommendations from Cramer: On the show Mad-Money (CNBC) Jim Cramer picks stocks which he recommends to buy.

The Cramer-effect/Cramer-bounce: After the show Mad Money the recommended stocks are bought by viewers almost immediately (afterhours trading) or on the next day at market open, increasing the price for a short period of time.

How to use this repo

- Automatic data scraping (with Github Actions): Every day at 00:00 the

scrape_mad_money.pytool runs and commits the data (if there was a change) to this repo. Feel free to use the created.csvfile for your own projects- (Why do we scrape the whole data range every day?): This way we can see the changes from commit to commit. If anything happens which would alter the historical data, we would be aware.

- ("manual") Data scraping: Use the

scrape_mad_money.pyto get the buy and sell recommendations Cramer made over the years- Result is a

.csvfile which you can use

- Result is a

- Backtesting the buy calls: Use the notebook

mad_money_backtesting.ipynb- To add your backtesting strategy, go to the

backtesting_strategies.pyfile and implement yours based on the existing ones

- To add your backtesting strategy, go to the

Warning: code quality is just "mehh", I did not pay much attention here, this is just a quick experiment

Backtesting

In the notebook there are notes how the experiment(s) were conducted and facts, limitations about the approach. You can also add your own approaches.

Available Strategies:

BuyAndHold(and repeat)AfterShowBuyNextDayCloseSellAfterShowBuyNextDayOpenSellNextDayOpenBuyNextDayCloseSell

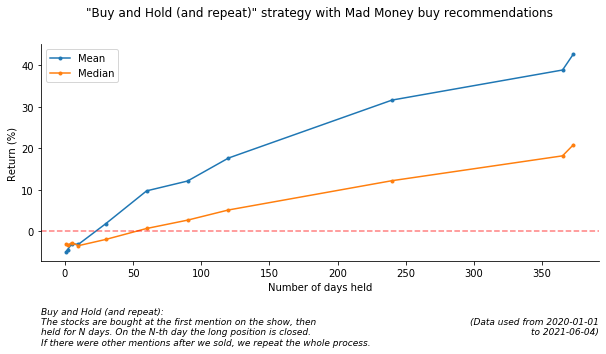

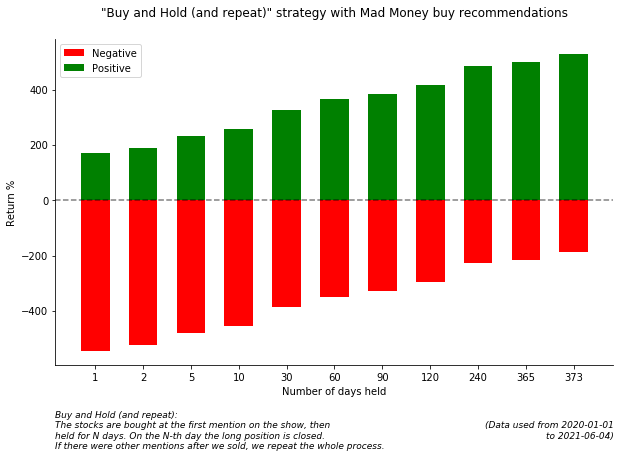

Buy and Hold (and repeat) Results

How is this different from the real-life scenario?

We backtest each mentioned stock individually, then aggregate the results. We define a cash amount for each symbol separately (e.g. $1k) and not an overall budget. This change should not alter the expected returns (in %) much if we assume you have infinite money, so you can put your money in each of the mentioned stocks every day.

As we don't have (free) complete after-hours trading data, the scenario when we "buy at the end of the Mad Money Show" is approximated with the value of the stock value at market close. This obviously alters the end result for the short term experiments if a stock has high daily volatility and it changes a lot afterhours. (Of course the "buy at next trading day open" is not effected by this, only if we count on the after hours data).